What Rising Prices Mean For The Market (And The Yields You Need To Earn…)

Whether it’s a new pair of shoes or a trip to the grocery store, things are suddenly costing more.

The biggest sticker shock might be at the used car lots, where pre-owned vehicle prices just experienced the biggest monthly increase since record-keeping began in 1953. Driving them isn’t getting any cheaper either, given the 49% rise in gas prices over the past year.

A few weeks ago, we talked about the relentless 250% surge in lumber prices. Before that, I covered the powerful rise in copper and other base metals. And, as my readers well know, both of these fit into my argument that we’re in the early innings of a commodity “super-cycle”.

These are by no means isolated examples. Steel prices jumped 18.4% just in the past month. Plastic materials are getting more expensive. So are dairy and meat products. Chicken wings have recently doubled from $1.50 per pound to $3.00 per pound due to shortages – get ready for higher menu prices at your favorite sports bar.

So what’s going on here?

The Bigger Picture

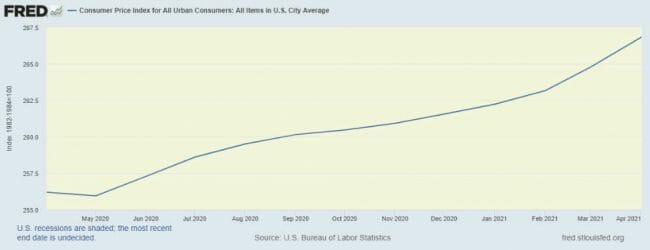

We can take some of these year-over-year figures with a grain of salt, considering the economy was in lockdown mode 12 months ago. Buoyed in part by stimulus check spending, the supply/demand imbalance is viewed by some as transitory rather than permanent.

Still, ignore the chart below at your own peril.

Source: FRED

Even more alarming is what’s happening at the wholesale level. The producer price index (a closely-watched gauge of what manufacturers pay for raw materials) jumped 6.2% last month, accelerating from March’s 4.2% uptick. Once again, that’s the sharpest increase ever recorded.

All of the inputs I just mentioned (and more) factor into the costs consumers pay. Some will be absorbed – but many will be passed through. As I informed readers of my Takeover Trader letter last week, I am starting to see the word “inflation” creep into one earnings call after another. In fact, it has been mentioned by at least 175 major companies over the past few weeks.

Take General Mills, for example, whose portfolio includes Cheerios, Pillsbury, and Haagen-Dazs ice cream. When discussing pinched profit margins, management noted “we are seeing rising cost pressures and increased costs to serve. The inflation is broad-based, we see it in grains and logistics.”

It’s not just ingredients, but also manufacturing (often energy-intensive), packaging, and transportation. Put it all together, and the cost of doing business has forced companies to take action. Procter & Gamble is hiking the price of Pampers diapers. Smucker is doing the same with Jif peanut butter. And Whirlpool is upping the price of home appliances.

Could this latest bout of inflation be just a head-fake? Possibly. It may not fully stick. But with the dovish Federal Reserve keeping short-term rates near zero and running the printing presses at full speed, it’s a matter of when, not if.

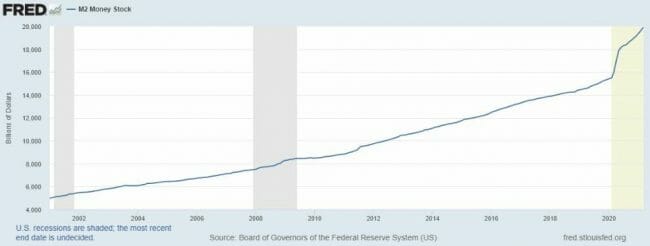

To counter the impact of the pandemic and stimulate the economy, the central bank has been purchasing government bonds and other securities on an unprecedented scale, pumping $120 billion per month into the system. The M2 money supply (which includes physical notes in circulation, savings accounts, and bank reserves) surged from $15 trillion at the start of 2020 to nearly $20 trillion today.

Source: FRED

That means one-quarter of all greenbacks have been newly minted within the past 12 months. In percentage terms, we haven’t seen a flood of new money like this since 1943 in the middle of World War II. And there are other factors in play this time, namely production shortages brought about by the prolonged shutdown of the global economy. Case in point: order backlogs and long wait times for new shipping containers. Or the severe lack of new homes as construction ground to a halt.

Fed Chair Jerome Powell has acknowledged these supply bottlenecks, but the central bank is stubbornly keeping the monetary needle pointed firmly towards the “accommodative” setting.

At least for now.

The Market Reacts…

For their part, traders appear to be convinced that inflation is here to stay. The breakeven rate on 10-Year Inflation Protected Treasuries (a proxy for inflation expectations) hasn’t been this high since 2013. If these numbers persist, the Fed will be compelled to start winding down or at least tapering its bond purchases to cool things down.

Minutes from the last Fed meeting already reveal a simmering debate among board members on when it might be time to switch policy gears.

Remember the last “taper tantrum”? A repeat would lead to soaring bond yields… and potentially a 20% correction in stock prices, equivalent to a 6,000+ point decline in the Dow. Incidentally, that event also took place in 2013, the last time inflation expectations reached this level.

And it’s not just the United States. Along with our Federal Reserve, quantitative easing programs by the European Central Bank (ECB), the Bank of England, and the Bank of Japan have bloated their combined balance sheets by $25 trillion. We needed that monetary medicine a year ago, and weaning the market off this juice is never easy. But the combination of supply constraints and runaway government spending will eventually lead to a day of reckoning.

Some fear that the Fed may wait too long to take pre-emptive action to forestall inflation. By then, it may be too late. Once unleashed, it’s difficult to bottle up – have you ever tried putting toothpaste back in the tube?

Action To Take

I’ll have much more to say on this topic in the coming days. I’ll also discuss some practical steps you can take to combat (and even profit from) the effects of inflation. So stay tuned.

I’ll also reiterate my recommendation of Blackrock Resources & Commodities Trust (Nasdaq: BCX). This is a fund we added to our High-Yield Investing portfolio back in February. We’re already up by about 12% on it… but there could be a lot more upside ahead if inflation truly takes hold and my commodity “super-cycle” prediction plays out.

In the meantime, the fund pays a yield of nearly 5% — which can go a long way toward protecting your portfolio and providing investors with the income they need.

For now, just know that there is no reason to panic just yet. If you’re near or in retirement, then you already know that earning solid yields (particularly from companies that historically reward shareholders with rising dividends) is one of your best weapons.

That’s also where my High-Yield Investing premium service comes in. You don’t have to settle for low yields – even in a low-interest environment. We’re finding yields of 6%, 7%, 9% and more from reliable securities that most people don’t even know exist.

To see our our latest research, check out this special report here.