These Unique Securities Allow You To Profit From Rising Rates…

You gotta hand it to them, it’s good to be a banker.

Aside from getting an inordinate number of paid holidays (Columbus Day, Flag Day, Arbor Day), you must admit they have a pretty great business model. My local branch pays 0.06% to savings-account depositors and then immediately loans out the proceeds to home buyers at around 5% — or credit card holders at 18%.

Multiply that by tens of thousands of customers, and pretty soon you’re talking about real money.

It’s a good time to be a lender. But you don’t rack up profits like that by being overly generous. Even after a couple of interest rate hikes, the average rate on a 2-year CD is still an anemic 0.27%. But fear not, there’s a way to put yourself on the other side of the table.

If you don’t like the idea of settling for what the bank gives, then invest in what it receives…

Your Chance To Be The Banker

You might have heard of bank loan funds. They are sometimes referred to as senior loans, prime rate loans, syndicated loans, or floating-rate loans. Whatever you call them, they can help buoy your portfolio over the next 12 to 18 months.

So how can individual investors participate in bank loans? Well, once upon a time this asset class was only open to hedge funds and other institutional investors. But since the 1990s, a variety of mutual funds, closed-end funds and even exchange-traded funds (ETFs) have been launched with the sole purpose of holding packaged pools of bank debt.

These loans are typically made to sub-investment-grade companies with less than stellar credit. Because the borrowers don’t have the strongest balance sheets, there is some credit risk involved. But that risk is mitigated by two factors…

First, the lenders are protected by restrictive covenants, which prevent the borrowers from taking any action that the bank feels is detrimental to getting its principal back. Second, whereas most bonds are unsecured, these are backed by tangible collateral such as property, equipment and inventory.

As the senior lender, the bank originating these loans is entitled to recover its money ahead of other creditors in the event of non-payment. So, it’s first in line. But that’s normally not an issue, because defaults are pretty rare, running around 2% for the S&P/LSTA Leveraged Loan Index.

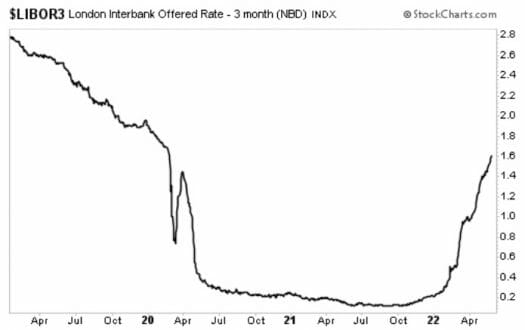

Even then, a Moody’s 15-year study found that recovery rates average 80.3%. That means even the few loans that go belly-up still return 80 cents on the dollar after assets are liquidated. But what really makes this group shine in the current environment is that the rates on these loans are variable (or floating) rather than fixed. Most are linked to a short-term benchmark such as the London inter-bank offered rate (LIBOR) plus an extra 4%.

The 3-month LIBOR has risen dramatically in recent month, from a low of 0.2% in January to 1.6% in May, meaning many bank loans are now paying 5.6%. And if short-term rates continue to rise, so will bank loan yields — considering their interest rates reset every 30 to 90 days.

Of course, the reverse is also true in a falling rate environment. But the odds of a rate decrease anytime soon are slim to none.

Make Rising Interest Rates Your Friend

With a traditional corporate or government bond, you are locked into a fixed coupon rate for the life of the instrument. As such, holders can only watch helplessly as interest rates rise and they’re locked in for the next five or 10 years. They are faced with an unpleasant choice: stick with the below-market rates until maturity or sell the bond early for a loss.

By contrast, yields on outstanding bank loans ratchet higher within a matter of days. These funds can also reinvest distributions into new securities with higher yields, thereby generating stronger distributions for shareholders.

So this asset class isn’t just immune to rate hikes — it actually welcomes them.

And keep in mind, we’re still emerging from the lowest rates on record. It will take another several more hikes from the Fed for rates to even begin to resemble what we normally see in a healthy economy. The benchmark 10-Year Treasury at 2.8% is still near the low end of the historical spectrum.

So, with muted credit risk and almost zero interest rate risk, bank loan funds are remarkably stable even in tumultuous times. There have been stretches in previous years where net asset values (NAVs) went months without deviating by more than a few pennies per share in either direction.

Closing Thoughts

There’s a reason why variable rate mortgages scare the heck out of people. The higher and faster rates rise, the more interest you pay to the bank. Bank loan funds allow you to turn the tables and flip that scenario.

Here are some names to consider:

– Nuveen Floating Rate (NYSE: JRO)

– First Trust Senior Loan ETF (NYSE: FTSL)

– SPDR Blackstone Senior Loan ETF (NYSE: SRLN)

Even if rates stay flat, these funds still offer enticing yields. JRO, a previous pick I’ve made for premium readers, yields nearly 8% right now. That blows a 10-year Treasury out of the water — and you don’t have to tie up your money until 2032 to get that rate — you can leave anytime.

Bottom line, any investor who’s worried about rising interest rates and wants to earn a solid income stream should be looking at bank loan funds.

In the meantime, if you’re looking for a way to earn higher yields in this low-rate market, then you should check out my latest research…

In it, you’ll find 5 “Bulletproof Buys” that have weathered every dip and crash over the last 20 years and STILL hand out massive gains to investors. With picks like this, you can “keep it simple”… In fact, you may never have to worry about what the market is doing again!