This Might Be My All-Time Favorite “Bet With The House” Stock…

It’s one of my favorite ways of looking at the market and picking an investment.

“The house always wins.”

It’s an idea that we all know, yet few seem to understand outside of whenever they visit the casinos in Las Vegas.

But you’ll go far if you can grasp this concept and apply it when looking for investments.

Betting with the house just seems to work year after year.

2 Businesses Where The House Always Wins

I talk about this idea regularly with my premium readers over at Capital Wealth Letter. We hold a few stocks that follow this idea. And when I talked about this last year, I mentioned one business where this concept is illustrated perfectly: credit cards.

For example, think of the credit card company, Visa (NYSE: V). Every time you swipe your Visa card, the merchant must pay a small transaction fee to Visa for facilitating the purchase.

In a way, Visa is the house. It doesn’t matter if the consumer is in a good mood or a bad mood. It doesn’t matter if they’re flush with cash or on the verge of bankruptcy. The house always gets its cut.

Another area where we can see this at work is with insurance.

There’s a reason why this is Warren Buffett’s favorite business. I explained how the insurance industry works in this piece:

Insurance companies can turn a profit through what’s called a float. A float is the premiums an insurer collects but has not yet paid out in claims. And this hoard of cash can grow large for insurance firms. For well-run ones, it’s also a powerful tool for generating profits. But this is where it can trip up many investors because float actually sits on the balance sheet as a liability, on the premise that the cash could be paid out as claims someday.

But here’s the kicker: in reality, the float is an asset. The premiums that an insurer collects, or float, are held in trust to pay future benefits or claims. So for accounting purposes, yes, it’s a liability since this money might have to be paid back at some unknown point in the future. But this isn’t just cash sitting idle in a bunker waiting to be deployed. This is money that can be invested, and any income and capital gain are kept by the insurance company.

As I’ve said before, insurance may seem boring, but it is a beautiful business. It’s no wonder that it is the real secret behind Berkshire Hathaway’s success. We own a couple of insurance names over at Capital Wealth Letter, and they’ve both crushed the market during the time we’ve owned them.

This Might Be My Favorite “Bet With The House” Stock

Today, I want to update you on a stock I’ve mentioned before that fits perfectly within this “bet with the house” idea.

I’m talking about CME Group (Nasdaq: CME).

This is one of my all-time favorite stocks. Here’s why…

When you place a trade to buy a stock, your broker routes that order to a marketplace with a seller. Then, your broker will pay a transaction fee to that exchange for providing liquidity and a marketplace for that transaction.

Every day, CME is the intermediary for millions of options and futures contracts. It’s the “house.” Traders may make a fortune, eke out a few pennies here and there, or lose everything. It doesn’t really matter. Either way, CME takes a cut.

The beauty of providing a marketplace for these transactions to take place is that it’s also extremely profitable. The only thing that’s changed over the decades is the diversity of product offerings. This now-global trading platform offerings span interest rates, equities, foreign exchange, agricultural commodities, energy, and metals.

Numbers To Know

The company reported fourth-quarter and full-year results on February 8.

During the fourth quarter, the company pulled in over $1.2 billion in sales, which missed estimates by only $3 million. Earnings per share were $1.92, which beat by four cents. CME Group generated over $5 billion in sales and nearly $2.7 billion in net income during the year. That’s a year-over-year improvement of 7% and 2%, respectively.

CME can produce consistent and reliable income, but it’s rare for a firm like this to produce record-breaking sales or cash flow. That’s okay, though, because there’s plenty to go around, so CME gives that cash back to shareholders through dividends and special dividends.

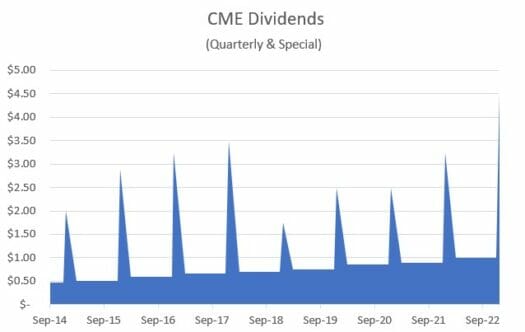

The company boosted its annual dividend by 10%. Its $4.40 yearly dividend will be paid in quarterly installments of $1.10 per share. (To collect this dividend, you need to own shares before March 9.) That gives the stock a headline yield of about 2.4% right now. But there’s more…

On top of its regular dividend, CME Group also dishes out a special dividend every year, which has historically been pretty hefty. For example, its last special dividend, which pays every December, was $4.50 per share, more than its regular annual dividend of $4.00 per share in 2022.

I’m not guaranteeing anything here. But unless something catastrophic happens, you can probably count on double the income with this stock.

Action To Take

Over at Capital Wealth Letter, we’ve owned CME since August of 2014. You can see how well that’s worked out for us in the chart above…

We’re up more than 200% on CME, compared with the S&P 500’s 107% return during that time.

You get this when you’re not only betting with the house – you are the house. It’s also why CME Group is one of my favorite stocks. Whenever it’s trading for a fair price, I pound the table for my followers to add it to their portfolio (or buy even more).

P.S. My staff and I have just released a report of “shocking” predictions for 2023 (and beyond)…

This report is easily one of the most hotly-anticipated pieces of research we release each year. And if history is any guide, it could be one of the most profitable things you read all year…

From the U.S. dollar to driverless trucks to breakthrough cancer treatments and more… If you’re looking for ideas that could turn a modest investment into a small fortune, this is where you’ll find it.