Did This Innovative Oil Producer Just Double Its Reserves?

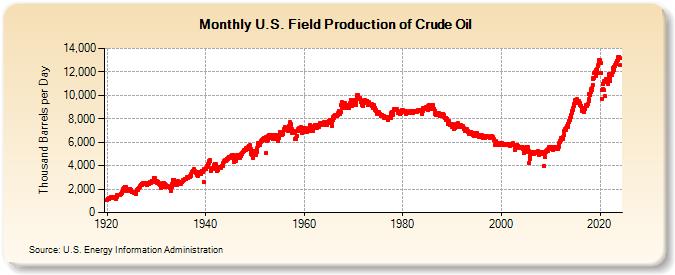

This month, the International Energy Agency released the 2013 version of its annual World Energy Outlook. Not surprisingly, the horizontal oil boom that has given birth to an oil production renaissance in the United States played center stage in the report.

However, some of what the IEA had to say about the U.S. horizontal boom may have caught some people by surprise.#-ad_banner-#

The IEA sees the horizontal boom making the U.S. the world’s largest oil producer by 2015. No surprise there — the media is all over that story.

But the IEA also said that the horizontal oil boom will peak by the year 2020. (But it’s only just begun!) After 2020, the IEA sees American production hitting a brief plateau before heading back into permanent decline. That doesn’t sound like an oil boom — in the grand scheme of things, it’s barely a blip on the long-term radar.

I don’t entirely agree with this view from the IEA, which I think massively underestimates the entrepreneurial spirit of the energy industry.

After all, the renaissance in U.S. oil production wasn’t led by supermajors like Exxon (NYSE: XOM) and Chevron (NYSE: CVX) — it was led by the independent producers that brought innovation and an entrepreneurial spirit to the problem of producing oil from tight and shale oil reservoirs.

While the supermajors were off looking for oil deep under the ocean and in unstable countries, companies like EOG Resources (NYSE: EOG) “cracked” the shale oil code back here in the United States.

Along with cracking the code, these companies also locked up big acreage positions in the best horizontal oil plays. That real estate is going to reward them for decades.

EOG has large land positions right in the heart of both the Bakken and Eagle Ford oil plays. Over the past five years, this has allowed for a great run of production and reserve increases for the company.

What I think the market doesn’t appreciate about EOG and other horizontal oil producers is that their best days are still in front of them.

This horizontal boom is still young, and the technology and techniques being applied are changing quickly. Given the amount of oil trapped in these horizontal oil plays, small improvements in technology and best practices can result in huge increases in the amount of oil these plays ultimately produce.

Let’s consider EOG and its Eagle Ford assets. Initially in 2010, with well results and technologies then available, EOG thought it would be able to recover 900 million barrels from its Eagle Ford acreage in South Texas. Things have changed since then.

Last year, EOG said that instead of 130-acre well spacing, the optimal well spacing will actually be 40 to 65 acres. More wells per acre means that more oil can be recovered. Thanks to this tighter spacing, EOG expects the amount of recoverable barrels in its Eagle Ford acreage will actually be 2.2 billion barrels — a mind-boggling increase of 1.3 billion barrels.

In the Eagle Ford, EOG is sitting on 27.9 billion barrels of oil. The initial assessment of 900 million recoverable barrels assumed a recovery factor of less than 4%. Even with disclosed increase to 2.2 billion barrels, that recovery factor is still under 8%.

For investors, the key is to focus on the companies that own the land that has the oil in place. EOG has a lot of that land and in exactly the right places.

Risks to Consider: The main risk to any commodity producer is the price of the commodity it produces. EOG’s revenues are weighted toward oil, so any drop in the price of that commodity will directly impact cash flows and reserve values.

Action to Take –> Buy shares of EOG Resources for long-term exposure to the huge amount of oil in place the company controls. The company trades at a very reasonable 7 times current earnings before interest, taxes, depreciation and amortization (EBITDA) and has a conservative debt-to-cash flow ratio of 1. Paying a reasonable valuation of current cash flow for a high-quality company with great growth prospects is just plain sensible investing.

P.S. Since we opened our doors, we’ve revealed literally thousands of investment opportunities. But there’s something we’ve never discussed before. It’s a triple-digit opportunity that our newest analyst heard about 10 years ago from his insider friends in Canada… but is available to all U.S. investors. Last year, you could have made as much as 139% in a little over a month. And in 2008, you could have made 73% or even 92%… all without day trading, buying or selling options, or doing anything bizarre. We’ve crafted a short document that will explain everything in full. You can access it free by clicking here.