My Favorite Way To Earn Tax-Free Monthly Income

Well, another tax season is upon us. Like many people, I tend to procrastinate until the bitter end, racing against the filing deadline to complete stacks of forms and triple-check all my figures. Fortunately, we’ve been given a little more time than usual for the past couple of years. Maybe next year I’ll get started early…

Either way, Uncle Sam always gets his cut. All of the dividends and interest received during the year were tallied up and listed on Schedule B. Same goes for the totals reported on lines 2 and 3 of my federal 1040. This is the place where all income investors must pay the piper.

I love seeing all those payments roll in. But this is the one time of year when I wish the dollar amounts on my 1099-INT and 1099-DIV statements were smaller.

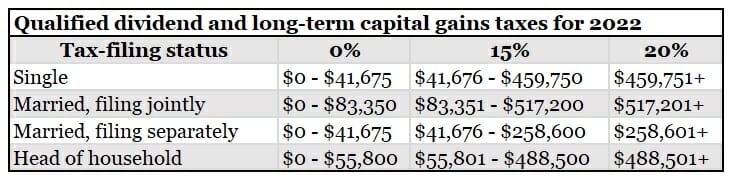

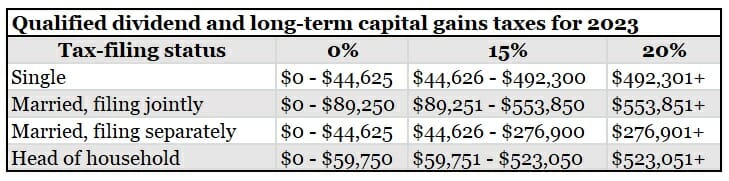

The sting may feel different, depending on your taxable income and filing status for the 2022 tax year. The tax rate on qualified dividends is 0%, 15% or 20%. (This is also the same rate for long-term capital gains.)

The tax rate on nonqualified dividends is the same as your regular income tax bracket. Some income qualifies for reduced rates (depending on the source). But other distributions are treated as ordinary income and fully taxed at rates up to 37%.

So if you’re an upper-bracket investor who received $10,000 in such payments, the government will be expecting $3,700, leaving you a net of just $6,300. You could wind up with even less once state taxes are imposed.

As they say, it’s not what you make that counts, but what you keep.

Muni Bonds: A Safe Way To Earn Income And Avoid Taxes

With that in mind, investors in the mid to upper tax brackets may want to consider shielding some income with municipal bonds. As you probably know, the interest from these securities is tax-free at the federal level. Bonds issued from municipalities within your home state are also exempt from state and possibly even local taxes as well.

Without getting into the nitty-gritty, municipal bonds are debt issued by states, cities, and agencies, often to raise money for public works such as new roads, bridges, schools, hospitals, and water treatment plants. They come in two main flavors. General obligation (GO) munis are backed by the full faith and credit as well as the taxing authority of the government that sold them. That means the issuer can always increase property or sales taxes if necessary to make sure interest and principal on the bonds is paid.

Revenue bonds are used to finance specific projects… airports, sports stadiums, toll roads — things like that. The revenue generated by these facilities is then used to repay the lenders over time. Revenue bonds are generally riskier, but also carry higher yields.

To compare the payout on a muni bond to that of an ordinary corporate or Treasury security, you need to determine its taxable equivalent yield (TEY). The calculation is quite simple:

Muni yield / (1 – Your Federal Income Tax Bracket) = Taxable Equivalent Yield.

(You can also find handy calculators online, like this one.)

Let Muni Bond Funds Do The Work For You

Muni bonds offer more than just tax perks. They are also guaranteed by trustworthy borrowers — some are even backed by private insurers, thus ensuring pristine “AAA” credit ratings. There have been a few high-profile bankruptcies, the largest being the city of Detroit in July 2013, in which investors were on the hook for billions in unpaid debt. But these are isolated incidents — muni bond defaults are incredibly rare.

With that said, most investors would probably be better off with bond funds than individual securities. All it takes is one troubled issue to wipe out years of gains on other holdings. Plus, the bid-ask spreads on individual bonds are often rather wide. As the “little guy” competing with large institutional investors, you will pay more on the entry and receive less on the exit, thereby reducing your effective yield.

Of course, there are other considerations, such as fees and expenses, performance, portfolio duration, use of leverage, and potential exposure to the alternative minimum tax (AMT). (As always, you should consult your tax professional for guidance.)

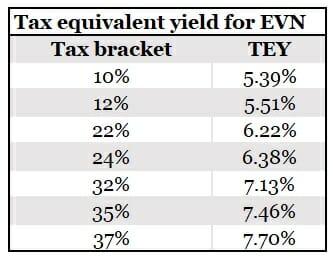

With that said, let’s use the popular iShares National Muni Bond (NYSE: MUB) for an example, which holds more than 3,000 bonds from across the country. MUB has a current distribution yield of about 2.2%. That’s not terribly exciting. But remember, Uncle Sam doesn’t take a bite.

So the Taxable Equivalent Yield for an investor in the top tax bracket is 3.5%. In other words, an ordinary bond fund would have to pay at least 3.5% to match MUB’s 2.2% yield after taxes. Using the same math, a muni bond fund paying 3.5% would have a Taxable Equivalent Yield of 5.56%.

Of All The Muni Bond Funds, This Is My Favorite

There are hundreds of options for investors when it comes to choosing muni bond funds… Mutual funds, exchange-traded funds, and closed-end funds (CEFs). In general, I prefer the closed-end route for this particular asset class. It can be somewhat illiquid, but trained analysts can spot changing credit qualities and take advantage of pricing inefficiencies. CEFs also generally offer richer payouts, and many trade at attractive discounts to their net asset value (NAV).

If I had to pick a favorite, I’d give strong consideration to Eaton Vance Muni Income (NYSE: EVN). The five-star fund (rated by Morningstar) invests in muni bonds representing dozens of carefully-screened issuers, most of which are backed by strong AA and AAA borrowers to pay for hospitals, mass transit projects, and water/sewer system upgrades. Average maturities and duration fall in the intermediate range, giving the portfolio higher returns than short-term funds, with less interest rate sensitivity than long-term options.

These holdings support monthly distributions of $0.049 per share, for a yield of nearly 5% at recent prices. That’s equivalent to a taxable payout of nearly 8% for investors in the top tax bracket. And the fund is currently trading at a discount of 11.7% to its net asset value (NAV).

While a bit more expensive than passive ETFs, the well-managed fund has been worth every penny. Average returns over the past decade rank in the top 1%, meaning it has outperformed 99% of its category rivals.

Closing Thoughts

Remember, there isn’t any benefit to holding munis in an IRA. So muni bond funds are best suited for a regular (non-IRA) account. Consult your own tax professional for guidance. (With that said, on a related note, I wrote about the benefits of the Roth IRA here.]

As always, you should do your own research in this space before deciding what’s right for you. That being said, EVN is a compelling option for anyone seeking steady, tax-exempt monthly income. That’s why it’s a member of our portfolio over at High-Yield Investing, my premium newsletter service.

Either way, muni bond funds can be an excellent way to lower your tax liability and keep more of what you earn. The higher your tax bracket, the more valuable they can be to achieving your financial goals.

In the meantime, if you’re looking for more ways to get paid monthly, I’ve put together an exclusive presentation that reveals 12 of the most generous income plays on the market today.

Most investors looking for income think they have to settle for quarterly dividends. But there are plenty of high-yielding securities out there that pay you monthly — you just have to know where to look.

Better yet… these stocks pay out 4X more often than “normal” dividend stocks… putting money back in your pocket — faster.