As We Head Into The New Year, Keep An Eye On This…

The average household is expected to spend $1,436 on Christmas gifts, travel, and entertainment this year, according to accounting firm Deloitte.

The majority of those transactions will be rung up on credit cards. You can bet that many shoppers will experience something of a hangover in January when Visa and Mastercard statements start hitting mailboxes.

And considering average credit card interest rates range from 12.99% to a punitive 24.99%, those who only make the required minimum monthly payment might not reach zero balance until sometime in the year 2047.

Ok, that might be a slight exaggeration. Still, we all know the dangers of excessive debt. When used properly, bank loans and private lines of credit can be powerful tools. But they can also be unwieldy. All too often, borrowers get in over their heads and buried by a landslide of interest charges.

Digging out of that hole isn’t easy. Just look at Uncle Sam, who has accrued $22 trillion in public debt that must eventually be repaid. According to the Congressional Budget Office (CBO), the interest payments alone will total about $413 billion this year, consuming a good chunk of the federal budget.

Source: Federal Reserve Bank of St. Louis

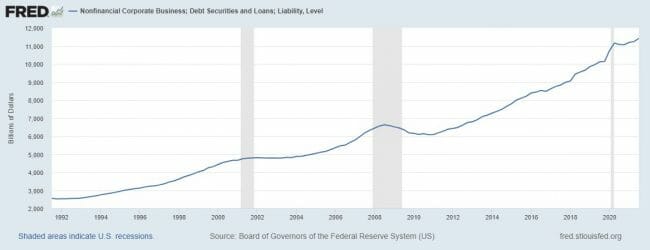

Corporate America Is On A Borrowing Frenzy

Maybe Washington can ask Apple (Nasdaq: AAPL) for a loan. The iPhone maker has accumulated $195 billion in cash. Yet, it’s still actively borrowing, announcing another $6.5 billion bond issuance a few months ago. That cash will be used, in part, to fund stock buybacks. Apple now carries about $114 billion in debt.

You can’t really blame the firm’s CFO for taking advantage of today’s historically low rates. The cheaper the cost of capital, the easier it is to deploy the proceeds somewhere that will earn even more, creating shareholder value. In this case, the hurdle can be easily stepped over, considering Apple is locking in rates as low as 1.4% on IOUs that won’t mature until 2028.

Shrewd.

Of course, it helps when you are a creditworthy borrower with an investment-grade rating. But those with a few dings on their credit report have also been able to tap into low-cost funding sources. The average junk bond yield is around 4.5% right now (half the historical average of 9%). That means even the shakiest borrowers are still paying less than what AAA-rated companies have been charged in years past.

Cheap money can be intoxicating. And corporate America has been imbibing heavily. That was the case long before the pandemic, but last year’s lockdowns only accelerated the process. According to the Wall Street Journal, U.S. companies (excluding banks) issued $1.7 billion in new bonds last year, raising their combined debt level to $11.2 trillion.

For perspective, that’s more than the GDP of every country on the planet except China and the United States. It’s more than the annual economic output of Japan, Germany, and India combined.

Much has been made of the fact that S&P 500 companies hold $2.7 trillion in cash. But they are also saddled with four times that much debt. For some reason, that doesn’t seem to get much attention among financial media outlets.

Source: Federal Reserve Bank of St. Louis

This influx of cash has, in some cases, provided a lifeline to keep struggling businesses afloat. You can understand why Delta Air Lines (NYSE: DAL) has ballooned its debt to $35 billion. Or why mall operator Simon Property Group (NYSE: SPG) issued fresh senior notes earlier this year to refinance older unsecured loans and stretch out the maturity dates. It was a no-brainer.

But prosperous companies (like Apple) are also getting in on the act. Amazon (Nasdaq: AMZN) certainly doesn’t need to borrow. The company has a record-high cash stockpile of $73 billion and pocketed another $4.9 billion in operating profits last quarter. Yet, it still held its second-biggest bond sale on record not long ago, borrowing another $18.5 billion.

Why not? That cash cost less than one percentage point above comparable U.S. Treasuries, a rock-bottom spread. And the proceeds will be used to build new warehouses, cloud-computing data centers, and other facilities to fuel future growth.

Companies like Wal-Mart and Home Depot are doing the same. In just one week back in September, 21 investment-grade businesses tapped the credit markets in what Bloomberg referred to as a “storm”. Deal volume for the busy month topped $130 billion.

Borrowing Rates Will Go Up…

As an optimist, I would say that this cash will be used to cover dividends, share buybacks, acquisitions, and a host of capital spending projects to stimulate growth. But eventually, the bill for this unprecedented borrowing will come due. And in the meantime, ask yourself this question…

What happens when interest rates begin to rise?

It’s only when the tide goes out that you learn who’s been swimming naked.

— Warren Buffett

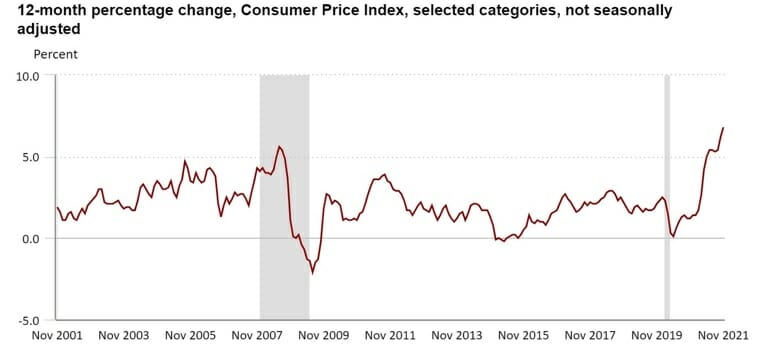

Fed Chief Jerome Powell has finally conceded that inflation isn’t a transitory illusion but instead is a real problem. It’s about time. I’ve been saying that since May. Just recently, we saw the hottest Consumer Price Index (CPI) reading since 1982. Prices haven’t been climbing this fast since Indiana Jones and the Raiders of the Lost Ark was playing in theatres nearly forty years ago.

Source: Bureau of Labor Statistics

This means rate tightening is only a matter of time.

Don’t just take my word for it. Powell himself has gone on record predicting the central bank will raise rates in 2022. And not just once or twice – but potentially three times. That’s a big deal for consumers. An extra 1% increase on a mortgage loan for a $200,000 home can add $100 to your monthly house note – or $36,000 over the life of the loan.

So imagine the financial impact of a business looking to borrow $200 million. Or $2 billion.

Closing Thoughts

There is an $11 trillion tidal wave of debt coming due in the years ahead. Servicing and refinancing those loans (to say nothing of raising fresh capital) is about to get far more costly. Make no mistake, it will sink some businesses. Expect to see the market scrutinize corporate balance sheet health far more closely in 2022 than it did in 2021. This will be a key factor separating winners from losers.

And this consideration is arguably even more important for income seekers. During times of economic distress, looming debt maturities will often take precedence over dividend payments, especially if available pools of capital dry up. It may not even be voluntary. Lenders often insist on protective covenants that limit or even restrict borrowers from making distributions.

That’s why my first recommendation for the new year over at High-Yield Investing is a business that has made tremendous strides at cleaning up its balance sheet. If there were a most-improved award, this company would take home the trophy. With its newfound financial health, this lean business has just tripled its dividend over the past six months – with another increase likely on the way.

If you’d like to learn more about this pick, then I invite you to give my service a try. You’ll also receive my latest report, which covers 5 “bulletproof” income-payers that have increased dividends for decades, no matter what’s happening in the market.