Here’s A Little-Known Way To Earn More On Your Savings, Risk-Free…

Cash doesn’t get the credit it deserves.

It’s the easiest way to reduce risk in your portfolio. Not only can it cushion your portfolio during a market crash, but it buys you freedom. I’m talking about freedom from worry – but also the freedom to act decisively on opportunities that have yet to come.

I’m not going to try and convince you to allocate a portion of your portfolio in cash today. I’ve already written about that several times. Instead, I want to address a common problem I see when investors are holding cash… they don’t know what to do with it.

To be honest, there are so many options out there… Savings accounts, money market accounts, certificates of deposit (CD), and more. It can be confusing.

It’s easy to see why investors leave their money parked in their brokerage sweep accounts or a savings account at their local bank. But it doesn’t have to be that way.

Better Than CDs, Money Markets, And Savings Accounts…

Before I started managing money for clients, I would hear folks talk about cash and the “risk-free rate” of Treasury Bills (T-Bills). I thought the only way to buy T-Bills was through a bank or mutual fund or some other financial institution. But that’s not the case… I’ll tell you exactly where I invest my cash that cuts out the middle-man, like banks, and their fees.

First, let’s look at the national average of interest earned in savings accounts, money market accounts and 1-year CDs. After all, with the Fed increasing interest rates, you should be getting a better return on that cash parked in your savings account, right?

That doesn’t seem to be the case…

According to the Federal Deposit Insurance Corporation (or FDIC — the entity that insures the money in your bank accounts), the national average interest rate paid on savings accounts is a meager 0.10%. Money markets pay 0.12% while locking up your money for one year in a CD will net you 0.31%.

Meanwhile, after the most recent hike, the current federal funds rate is between 2.25% and 2.5% — the highest it’s been since 2019 (before the Covid pandemic).

Of course, you may see plenty of ads touting savings accounts with annual percentage yields (APY) of 1.5% or more. But it seems there are always hidden caveats, whether it’s an account minimum, or a promotional period, or you have to have a direct deposit.

Instead, I want to encourage you to consider buying T-Bills. These are short-term debt obligations issued by the U.S. government (and backed by the Treasury), with a maturity of one year or less.

You can buy T-Bills, Notes, and Bonds directly from the government through TreasuryDirect.gov. This website allows you to buy and redeem securities directly from the Treasury in paperless electronic form.

Few people know about this handy resource. But it’s worth considering. You do have to take a couple of steps to set up an account, but you can easily link your current bank account and brokerage account to TreasuryDirect.

One of the beautiful things about investing in T-Bills is that the interest is exempt from state and local income taxes (it’s still taxable at the federal level).

How To Buy T-Bills

Now before I go any further, let’s address a few things.

Using TreasuryDirect does require a little bit of work compared to letting your money sit in a savings account. Another thing is that you are bidding in an auction for these securities, so there are some things to understand, but I think it’s worth the effort.

The first thing you need to know is that Treasury Bills are purchased at a discount and redeemed at the full par value. So for each $1,000 worth, you’ll pay $990-something (depending on the interest rate) upon issue and receive $1,000 upon maturity.

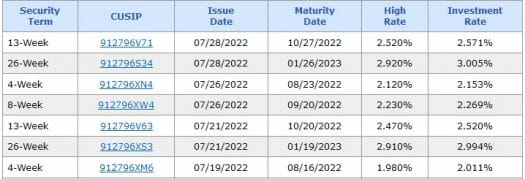

Rates are set by auction, so you won’t know your exact interest rate before you commit to buy. But here are some of the rates you can expect to earn based on recent data when I took this screenshot…

Source: TreasuryDirect.gov

As you can see, the recent results of the last two 4-week T-Bill auctions provided investors with an investment rate as high as 2%.

The 4-week T-Bill auctions are normally held on Tuesdays, and the T-Bills are issued and redeemed on Thursdays. TreasuryDirect also allows you to easily reinvest those funds into the next auction automatically if you would like.

Keep in mind that when you purchase a T-Bill, the money comes out of your account and will be gone during the investment period. So, I wouldn’t recommend purchasing a 4-week T-Bill using all of your funds. Leave a little cash in case you need to access it immediately.

Here’s an example of how I’ve personally done this to squeeze a little more out of my savings…

With about $50,000 sitting in a savings account at the bank, which is currently earning 0.1%, or $50 a year, I take between $40,000 to $45,000 and purchase 4-week T-Bills through TreasuryDirect. (You could opt for the 13-week or 26-week bills if the extra interest is worth locking up your money for that long – it’s up to you.) I like to leave between $5,000 and $10,000 in my savings account in the event of an emergency, or for personal spending.

By investing that $40,000 into T-Bills — and earning an interest rate double what my bank offers — I’m able to turn that $50 of annual interest into at least $800 (free of state and local taxes).

Closing Thoughts

I understand that this might be too much of a hassle for some folks. If your bank is offering you an interest rate near 2%, it might not be worth it. But as I mentioned, many banks require you to jump through just as many (if not more) hurdles for you to get their top rate.

With TreasuryDirect, you can purchase a T-Bill with as little as $100.

I know 800 bucks might not be much to some, but you have to remember that this is money that my family and I are not planning to do anything with, unless there’s an emergency. So this extra cash is risk-free. And with inflation soaring, I’ll take all I can get.

My advice: don’t wait for your bank to raise rates on their savings products. We’ve already spent the last decade-plus earning next to nothing on our cash. That no longer has to be the case. Take advantage of rising interest rates, and safely earn more on your money.

P.S. I’ve found the “next investment frontier” in technology — and early investors could make a killing…

I’m talking about the commercialization of outer space. It’s not as crazy as it sounds — and it’s all thanks to Elon Musk’s latest project, Starlink. It’s already rolling out across the globe, and it’s going to change the lives of millions of people (and make a fortune).

But there’s just one problem… It’s currently “off limits” to regular investors… Fortunately, we’ve discovered a little-known “backdoor investment” that can get you in on the ground floor, TODAY. (Without this “secret partner, Starlink will never get off the ground…)