Bonds 101: Bond Terms You Should Know (And Key Concepts)

If you consider yourself a serious income investor who also cares about capital preservation, you need to look at bonds. But first, there are some bond terms you should know before you get started.

Bonds, also known as fixed-income securities, are debt instruments created to raise capital. They are essentially loan agreements between an issuer and an investor, with terms that obligate the issuer to repay the principal at maturity and pay interest semi-annually.

Most self-directed individual investors have little knowledge of the bond universe. But ignoring this $127 trillion global market means you could miss out on significant income.

In this first article in a series, we’ll dive into the world of bonds. First, we’ll cover some basic bond terms you should know and discuss the relationship between price and yield. In a future article, we’ll explore bond ratings, different types of bonds, and their benefits and risks.

Bond Terms You Should Know…

Asset-Backed, or Secured, Bond

A secured bond, or asset-backed bond, is backed by collateral. The bondholder has the right to take possession of and sell this collateral if the bond issuer fails to make full interest and principal payments when they are due.

Callable Bonds

Bonds issued with call provisions can be redeemed, or called, at the option of the issuer before the maturity date. Issuers will often seek to redeem outstanding bonds when interest rates decline so that they can pay off the bonds and reissue them at a lower interest rate. The call price is usually above par, and the earlier the bond is called, the higher the price.

Callable bonds often carry a call protection provision, meaning there is a period during which the bond cannot be redeemed by the issuer. Call dates and redemption prices are disclosed to investors in the offering statement, and when a bond is called, the investor is notified by mail.

Commercial Paper

Commercial paper generally refers to short-term commercial loan agreements lasting three months or less. The term “paper” refers to the actual paper on which the borrower’s pledge to repay is printed. Most commercial paper is negotiable, which means it can be bought and sold like a commodity.

Although considered relatively safe, because it is issued by corporations, commercial paper is considered slightly riskier than 13-week Treasury bills. That means it usually carries a slightly higher interest rate.

Convertible Bond

A convertible bond allows the bondholder to exchange the bond for other securities at some future date and under prescribed conditions. In most cases, a bond will be convertible into shares of the underlying company’s stock.

Creditor

Bondholders are creditors who simply hold an IOU from the entity. This is in contrast to stockholders, who have equity or a unit of ownership in a company.

Debenture

An unsecured bond, or debenture, is backed by the full faith and credit of the issuer, but not by any specific collateral.

Face Value

Also known as “par value,” bonds are redeemed upon maturity at face value unless the issuer defaults. Face value is the amount on which interest payments are calculated.

For example, a 10% bond with a face value of $1,000 will pay bondholders $100 per year. Corporate bonds are usually issued with a face value of $1,000. Municipal bonds are usually issued with a face value of $5,000.

Fixed Income

Bonds are called fixed-income securities because they pay a specified interest regularly.

Interest Rate

A bond’s interest rate, or coupon rate, is the percentage of par (or face value) that the issuer is scheduled to pay to the bondholder annually.

For example, a $1,000 bond with a 3% coupon will pay the bondholder $30 per year, usually in six-month installments.

Bond issuers generally offer to pay an interest rate that is competitive with other bond rates at the time of issuance. Therefore, the rate is often similar to other interest rates, such as the prime rate, mortgage rates, personal loan rates, etc. Interest rates also vary based on other factors, the most important being the issuer’s creditworthiness.

Maturity

The maturity date on a bond indicates the date the borrower, or issuer, must pay back the investor’s initial investment. The bond is retired at the maturity date, and the borrower must repay the full amount of the loan.

Par

Par is equal to a bond’s face value, the amount to be repaid at maturity. When coupon bonds are issued, they are generally sold at par value.

Term

The life, or term, of a bond is fixed at the time of issuance. It can range from short-term (usually a year or less), to intermediate-term (two to 10 years), to long-term (10 to 30 years or more).

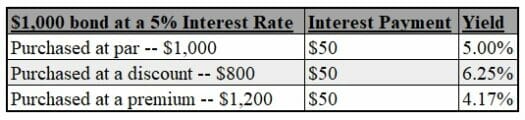

Yield

A bond’s yield usually differs from its coupon interest rate. Yield may be higher or lower than the bond’s stated interest rate (coupon rate). To determine the yield on a bond, simply divide the bond’s annual interest payments by its current market price. It’s important to understand that a bond’s yield varies inversely with its market price. As bond prices fall, yields rise. As bond prices rise, yields fall.

For example, if an investor paid $1,000 for a bond with a 4% coupon, the investor would receive $40 a year in interest. The yield would be 4%.

If the bond loses value and is sold for $800, the new buyer would still receive $40, but the yield would increase to 5%.

How yield changes:

Yield to Maturity

YTM is a precise calculation used to determine the annual rate of return an investor will receive if a long-term, interest-bearing security is held to the maturity date. The calculation considers the security’s purchase price, the time to maturity, the coupon yield, the redemption value, and the time between interest payments. Due to the complexity of the calculation, YTM is most often determined by using a bond calculator.

Conclusion

Bonds are debt instruments that provide a source of capital to issuers while offering investors a relatively low-risk investment opportunity.

This corner of the investment universe is often shrouded in mystery for the average investor. But if you’re looking for income, it’s a great place to start. What we have covered here are simply bond terms you should know — it is by no means exhaustive. It’s also important to understand the different types of bonds and the issuer’s creditworthiness before investing.

Stay tuned for our follow-up article, where we’ll cover these concepts.

In the meantime, if you want to know about our favorite high-yield picks, you need to check this out…

Forget meme stocks, crypto, and complicated trading strategies… The 5 safe, high-yield stocks in this report allow you to keep it simple…they’ve weathered every dip and crash over the last 20 years and STILL handed out massive gains.

They all have high yields, paying dividends that rise each and every year. You may never have to worry about what the market is doing again!