An Incredibly Simple (And Easy) Way To Earn 5% On Your Cash…

Here’s a question for you… When was the last time you logged in to your brokerage account to check to see if you have any uninvested cash?

Most people have some cash parked there — either as a matter of practice or neglect.

— It might be a deliberate asset allocation call (I’m keeping 10% of my money liquid in case of a pullback).

— It could be the proceeds from a stock sale, a recent deposit, or an account transfer that never got deployed.

— Or it could simply be accumulated dividend distributions piling up.

Whatever the reason, most of us have at least a little money sitting idle — few accounts are fully 100% invested. Unless you direct otherwise, uninvested cash is typically parked in something called a sweep account. Merrill Lynch and Smith Barney refer to it as a bank deposit program.

These accounts are safe (most carry FDIC and/or SIPC insurance) and liquid. But the rates they pay aren’t always competitive. Let me be blunt: they stink.

You’re Not Getting Paid Enough

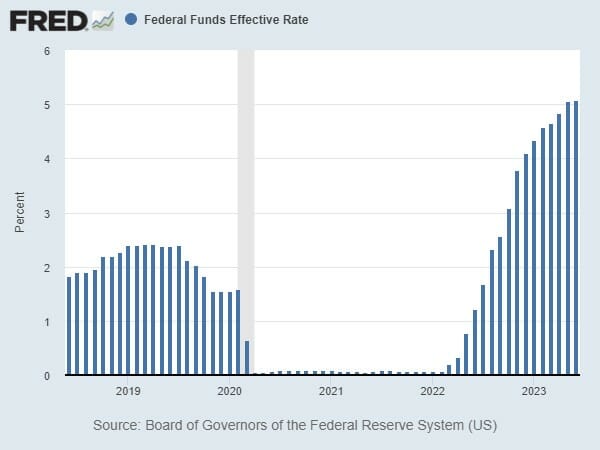

That was perfectly fine a couple of years ago when the Fed Funds Rate was anchored at 0.09%. Back then, replacement alternatives weren’t much better.

But as we all know, that was ten rate hikes ago.

Source: Federal Reserve Bank of St. Louis

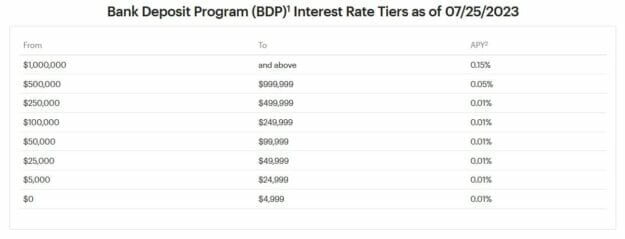

Sweep accounts aren’t terribly responsive to changing rate climates. Wells Fargo’s bank deposit sweep currently stands at a rock-bottom 0.15%. But there are breakpoints. You can get as much as 1.30%, provided you’re a top-tier client with $20+ million in assets.

That’s certainly not the case for borrowers, though. Credit card interest and variable-rate student loans adjust quite rapidly. But savers aren’t given the same treatment.

How is that possible with short-term rates screaming higher over the past 16 months? The last rate hike alone was a quarter point.

You’re Letting Them Get Away With It…

Bank-owned brokerages have financial reasons to favor one sweep option over another. They often funnel this unused cash to their parent, where it then becomes a low-cost pool of funding to support loan activities – and widen net interest margins. Some states have even launched probes into possible conflicts of interest and lack of disclosure.

The default sweep account at E*Trade is currently yielding 0.15%.

Schwab (which recently eliminated some of its higher-paying default options) is paying 0.48%.

No wonder Fidelity just called out its rivals for this practice. As of March, the nationwide sweep average is 0.43%, according to research outlet Crane Data.

When you manage billions in assets, every basis point saved means millions more earned. President Peter Crane summed it up nicely, saying, “brokerages have made a living picking up pennies that savers are too lazy to pick up for themselves.”

My message to you is: Pick up those pennies. They add up.

There are many reasons why brokerages are stingy with their sweep account rates. The simplest explanation: because they can be. After all, this isn’t a long-term obligation. Most investors consider it a temporary solution, so they don’t always shop for yield.

Money Market Funds: Earn More With Just A Few Clicks

As a bank investor myself, I certainly can’t fault companies for trying to sweeten the bottom line. But don’t let it be at your expense. There are better options, and moving your idle cash from one parking spot to another is a simple matter.

All it takes is a quick chat or a few buttons on the keyboard…

Over the past few years, the difference between sweep rates and money market rates has been negligible. But now, that spread is close to 400 basis points (4.39% average money market payout vs 0.43% average sweep rate). That’s a new record high.

In other words, never in recorded history has it been this advantageous to transfer your money from a sweep account to a money market.

On a $50,000 balance, that’s the difference between $215 and $2,195 in yearly interest income.

One caveat: money market funds (not to be confused with bank money markets) aren’t FDIC insured. But they invest in some of the safest, ultra-short term securities on the planet. Most safeguard their assets in Treasury Bills or repurchase agreements (collateralized loans to and from the Federal Reserve’s trading desk).

Money Market Funds 101

So-called prime funds take on a modicum more risk by investing in corporate-issued commercial paper and other high-grade financial notes, which aren’t backed by Uncle Sam and earn better rates. You’ll find that some money markets even focus on municipal securities that throw off tax-free income.

One thing they all have in common: stable net asset values. Most strive to stay at an even $1 per share at all times. Falling below (or “breaking the buck”) is a scenario to be avoided at all costs as shareholders would flee. When rates fell into the abyss, most issuers voluntarily reduced or waived their fees to keep NAVs at the dollar mark.

As long as NAVs stay level, your principal is safe. Combine that with rates now approaching (or even surpassing) 5%, and you can understand why assets have been flooding into money markets, driving assets to a record high above $5.4 trillion.

Picture this scenario.

A) A fund yielding 6%, but with the potential to lose 25% of its value in a down market.

B) A fund paying close to 5%, with negligible downside exposure.

Which risk/reward option would you find more appealing? Is that extra 1% worth the risk? If you said B, then you need to be invested in a money market. We can step over the same yield bar today that required quite a leap just a couple years ago.

If you appreciate stability, check out the historical price performance of almost any reputable money market fund. Actually, there’s no need. It’s just a straight horizontal line – no ups and downs. My recommendation over at High-Yield Investing hasn’t deviated so much as a penny, showing a 52-week high of $1.00 and a 52-week low of $1.00.

That wasn’t such an enticement a year ago when the yield was around 1% and just starting to climb – but now, at 5%, it’s speaking my language.

Closing Thoughts…

We spend most of our time here tracking down the best income-bearing securities over at High-Yield Investing. But as I’ve said before, asset allocation can have an even bigger influence on portfolio returns than security selection. And right now, cash is looking pretty good – not just because of macro uncertainties, but because other fixed-income classes are paying only slightly more with higher volatility.

My advice: don’t settle for your broker’s easiest cash management option. Consider putting a chunk of your cash into one of these high-yield money market funds. You’ll be glad you did. Not only will you be doing something productive with your cash, it’ll also help smooth out the rest of your portfolio.

P.S. What if I told you that instead of only getting paid four times a year from a stock… you could get 12 dividend checks a year?

It’s possible… you just have to know where to look. Over at High-Yield Investing, we own about a dozen — that’s 144 monthly payments a year! For the first time ever, we’ve compiled the full list into a report. Go here now for details.