Geopolitics Aside, There Are Plenty Of Reasons To Be Bullish About Energy…

The shocking attack on Israel by Hamas militants and powerful counterstrikes by Israeli forces have destabilized the Middle East.

Meanwhile, the conflict between Israel and Hamas (which has now claimed over 10,000 lives) isn’t letting up.

When footage of the atrocities perpetuated by Hamas was broadcast worldwide, it seemed crass to discuss stock prices amid such suffering. As a father, the barbaric treatment of women and children sickens me.

But the investor in me can’t help but notice the swift rally in defense stocks like Northrop Grumman (NYSE: NOC) and Lockheed Martin (NYSE: LMT). Even before, these companies had plenty of business on their plate. But both have gained ground since the attacks.

I’m a little more partial to Northrop, which has been awarded $15 billion in new contracts over the past 90 days and $34 billion for the year, raising the backlog to a record $84 billion. With many of its products rated “high priority” by the Pentagon, the bottom line is that advanced radar systems and hypersonic attack cruise missiles aren’t cheap.

The sector as a whole is worth a look.

Conflict Is Bullish For Oil, Too

Here’s another uncomfortable truth. These types of conflicts are generally bullish for oil and gas. Even before that, Vladimir Putin had been weaponizing energy across Western Europe following Russia’s invasion of Ukraine.

Meanwhile, on the supply side, OPEC recently throttled back on production again, slashing output by 1.3 million barrels per day. The cartel recently agreed to extend those cuts through the end of the year to keep supplies tight and prices firm. Predictably, the announcement triggered an immediate response from traders.

But let’s put geopolitics aside for a moment. The supply/demand picture also supports elevated prices – and thus increased output.

The world is thirstier than ever, with usage rebounding to a record 102 million barrels per day this year. The International Energy Agency forecasts that the total will climb by another million in 2024, bolstered by rising demand from the petrochemical and aviation sectors.

Even before that, steep industry down-cycles have discouraged large-scale exploration and development activity in recent years. Whatever the reason, the flood of surplus inventory has receded dramatically. In fact, the U.S. Strategic Petroleum Reserve (SPR), which was brimming with 638 million barrels in 2021, is now half-empty.

Put it all together, and you can see why forecasters like Goldman Sachs envision a scenario where prices could top $100 per barrel next year.

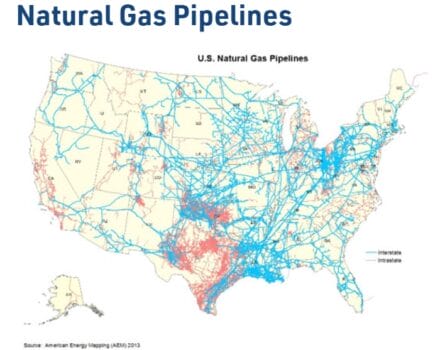

We Need More Energy Infrastructure

I’ve said this before, and I’ll probably say it again many times. We need more energy infrastructure in this country. It’s not only good for business – but it’s also a matter of national security.

As the world’s top producer, the U.S. will bring 12+ million barrels of crude oil to the surface today, along with 100 billion cubic feet of natural gas. The same again tomorrow. Moving those tremendous quantities out of remote fields to regional storage hubs and processing plants is a constant challenge.

At times, all of the available pipeline capacity in a given region is spoken for, forcing shippers to arrange alternate means of transportation, like trucks or railways. The pipeline deficits have grown so severe at times that drillers have deliberately chosen to leave new wells unfinished. As we speak, there are more than 4,000 drilled but uncomplete (DUC) wells nationwide.

In other words, logistical constraints have forced producers to purposely step on the brakes and curtail output. The addition of new pipeline systems in recent years has helped alleviate some of the congestion. But new capacity tends to be absorbed quickly.

There’s no quick and easy solution. These large-scale projects are costly and can take years to bring online. Future pipeline battles will be extremely contentious (and costly). At best, they will get bogged down by injunctions and protests that can take years to resolve. Others will be abandoned altogether.

All of this plays to the advantage of one midstream companies with expansive infrastructure (and customers) that are already in place.

A Ripe Sector For Deals

The upstream oil & gas sector is famous for its M&A activity — like Exxon Mobil’s (NYSE: XOM) $60 billion deal for Pioneer Natural Resources (NYSE: PXD). This is one we profited from immensely over at Takeover Trader, as you can see in the chart below…

But the midstream space is no stranger to deals, either. You can bet the macro factors I discussed above were a big reason why Oneok (NYSE: OKE) made Magellan Midstream Partners an offer it couldn’t refuse – to the tune of $18.8 billion.

The union of these two market leaders will create a $60 billion juggernaut with 25,000 miles of liquids pipelines and an unrivaled collection of complementary systems and networks stretching from the Gulf Coast to the Rocky Mountains.

I had a front-row seat to this spectacle because Magellan was a holding over at my High-Yield Investing service. The merger caused us to close out our longest holding (for a 600% gain, no less). And while I’m sad to see MMP go, I can’t help but feel bullish about OKE, given all of these macro factors.

Trust me, this won’t be the last deal we see in this space. Deals like this tend to lead to copycat deals – especially in the energy sector. That’s why I’m targeting another megadeal in the West Texas oil fields…

This little-known company is set to unlock the Mother of all Oil Booms. We’re talking about nearly a billion barrels of oil… just from one company. And in the coming days, it could unleash a surge of mega-profits. Click here for the full briefing now.