Use This Simple Strategy to Build Wealth in the Market

Do you want to know about a strategy that has the power to unlock amazing long-term returns…

Yet is so simple that anyone can use it?

We’re talking about dollar-cost averaging.

Yeah… we know what you’re thinking. Dollar-cost averaging sounds pretty boring.

But that’s why it’s such an underappreciated investing strategy. It doesn’t provide the same thrill that investing in a small-cap company might bring, but it’s a great strategy that deserves more attention than it gets.

It’s also nearly stress-free and will pay off greatly in the long run. It’s even historically proven to create greater wealth than a standard buy-and-hold strategy. In fact, the numbers we’re about to share with you about dollar-cost averaging are mind-blowing.

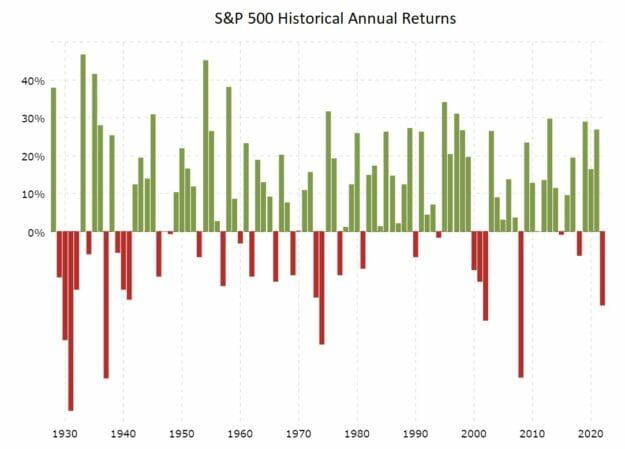

A Little History Lesson

First, let’s discuss the market’s historical performance. Now, the S&P hasn’t always been the S&P 500. The index started in 1926 with just 90 companies, expanding to 500 components in 1957. But it’s still a pretty good proxy for the overall “market.”

Since 1942, the market has been up during 64 years, including dividends. During this period, the average return for an up year was 19.1%. The average return for a down year was -11.7%. So not only does the market have a win rate of 80%, but when it wins it does so in a bigger way than when it loses.

Source: Macrotrends.net

In other words, losing money in the stock market long-term is rather difficult. Really, the only thing that gets in the way is our emotions.

When stocks head lower, typically, the media starts screaming at us that the world is about to end. So we sell our stocks.

On the flip side, as stocks climb higher and higher, we get FOMO (“fear of missing out”) and begin buying. This emotional tug-of-war cripples our returns, impeding the magical wealth-building apparatus that is the stock market.

And it’s here where dollar-cost averaging can turn things around for us.

The Numbers Don’t Lie

Imagine it’s the year 1999, and you’re gearing up to start investing. We are looking at a 15-year investment horizon, so from 2000-2014, and you will be investing $1,000 a month, every month during that 15 years.

Keep in mind this is going to be one of the worst investment periods for stocks. You’re investing at the height of the dot-com bubble and then will suffer through the financial crisis in 2008.

You have two investment choices.

You have two investment choices.

You can invest your $1,000 monthly allotment into the Vanguard S&P 500 fund or the Vanguard Short-term Bond Index fund.

During these 15 years, the Vanguard S&P 500 fund earned just a 4.1% compounded annual growth rate. Meanwhile, the Vanguard Bond fund also returned a 4.1% compounded annual growth rate. Except, the bond fund had zero down years. The S&P 500 had four down years — including the gut-wrenching 37% loss in 2008.

We would venture to guess that, given these choices, most folks would invest in the Vanguard Bond fund. After all, both returned the exact same amount, yet the bond fund didn’t have a single losing year, while stocks took you on an emotional roller coaster ride.

But again, this is where dollar-cost averaging really comes into play…

As it turns out, if you chose the bond index, your $180,000 cumulative investment turned into $228,294. Had you chosen the stock fund, however, your same investment would have swelled to $352,202. That’s an incredible $130,000 more than the bond fund.

Same exact returns, yet vastly different results. That’s the power of dollar-cost averaging.

Taking It To The Next Level

Using an approach like this touches on a major facet of investing… our emotions. If the market tumbles and we have a systematic approach to building wealth in place, then our mindset goes from one of fear (which often leads to panic selling) to one of encouragement.

That’s the part about dollar-cost averaging that we really like. But you can take it even a step further.

Imagine if you pair this simple approach with stocks that have the potential to really knock it out of the park…

Let’s say you own shares of a company that is creating some truly world-changing stuff… It could be a groundbreaking medical treatment, a new gadget that every consumer will want to own, you name it.

The point is, if it’s truly game-changing, you don’t have to bet the farm on it right away. This is where a strategy like dollar-cost averaging really begins to pay off.

Think about it this way. If you were fortunate enough to own a stock with the truly game-changing potential of an Apple (NSDQ: AAPL) or Netflix (NSDQ: NFLX), then we want to be in it for the long haul (obviously). And if a stock like this suffers a temporary setback, but the long-term picture remains in place, then we can rejoice instead of panic. We’re getting investments we want to own for less.

This gives us the chance to stay in the trade and have the opportunity to reap the amazing long-term returns that investments like this produce.

The Bottom Line

The point is that strategies like dollar-cost averaging allow us to focus on the bigger picture. Especially for those of us who want a chance to nab some truly life-altering gains from the innovation that’s happening around us every single day.

The list of game-changing opportunities never ends. In fact, in today’s environment — where information, ideas, and technology are spreading at the speed of light — the opportunities are greater than ever.

Think of everything we know today that has changed over just the course of a few years… we’re willing to bet you wouldn’t have thought half this was possible a little more than a decade ago.

If you’re looking for promising profit-making opportunities, consider our colleague, Nathan Slaughter, the chief investment strategist of High-Yield Investing.

For the last 16 years, Nathan has made it his solitary focus to help everyday Americans invest profitably for retirement.

As a high-yield expert, Nathan has devised a simple strategy that could help you generate a steady stream of cash, almost like clockwork. Click here for details.