How to Play the Buyout Game: 3 Tips For Finding the Best Deals

Philip Morris International (NYSE: PM) is one of the most controversial companies we cover.

I understand not everyone likes investing in cigarette manufacturers, and that’s fine…

But our job at StreetAuthority is to give you the most timely and profitable investment advice available.

In short… our job is to help you make money.

And in doing so, we wouldn’t be doing our job if we neglected to tell you that although it may be controversial, Philip Morris is also the most shareholder-friendly company on Earth.

In just four years, the company has raised its dividend 85% and bought back 467 million shares of stock. During that time, shares have returned roughly 100%.

Here’s how Philip Morris returns value to shareholders on a consistent basis…

First, the company buys back its own stock month after month — no matter what the market is doing. It’s bought back a staggering 22% of its shares in the past four years.

There’s no doubt that’s a major reason this “boring” cigarette company has been doubling investors’ money.

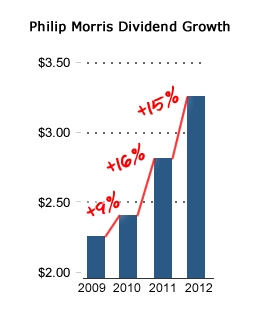

Philip Morris is one of the exceedingly rare companies that consistently grows its dividend year after year.

Since the company paid its first dividend of 50 cents per share in June 2008, it has raised its dividend every single year.

Take a look at the chart of Philip Morris’ dividend growth to the right…

And I expect this rapid dividend growth to continue for years to come.

Since spinning off from Altria (NYSE: MO) in 2008, Philip Morris has quickly amassed a $4.8 billion “Dividend Vault.”

A “Dividend Vault” refers to the enormous stockpile of money a company uses to pay dividends to shareholders.

With billions of dollars sitting in its “Dividend Vault,” Philip Morris should have no trouble paying a steady, growing dividend well into the future.

Looking forward, despite its size and industry dominance, Philip Morris still has plenty of room to grow.

Remember, Philip Morris is a spin off of Altria’s cigarette business. But there’s a big difference between the two companies.

While Altria continues to sell its brands, including Marlboro and Merit, in the United States… that business is slowly shrinking.

Philip Morris, on the other hand, focuses outside the United States. And in the international markets, it’s a very different story…

Overseas markets offer greater growth opportunities in the cigarette industry because of their growing populations and looser restrictions on tobacco marketing. There will be an estimated 1.4 billion smokers globally by 2020, up from 1.3 billion today — that’s an additional 100 million potential customers, many of whom will choose a Philip Morris brand.

In fact, Philip Morris sells its products in 180 countries and owns seven of the world’s top 15 brands.

Philip Morris is exactly what I look for in a shareholder-friendly business. It buys back shares, consistently raises dividends, owns an enormous “Dividend Vault” and has tremendous growth potential.

It’s a rare thing whenever you find a company that possesses all of these traits. But when you do, you don’t want to pass it up.

Risks to Consider: Of course, there’s no quality a company can possess that will guarantee its success. But when you can find companies like Philip Morris that dominate their market and are returning billions to investors, these are the sort of stocks that can deliver strong returns in nearly any market — including this one.

Action to Take –> I recommend buying the stock up to $85 a share with a price target of $115 a share.

P.S. — Philip Morris is just one of 13 stocks I’ve discovered with an enormous “Dividend Vault.” Right now, U.S. companies own a “Dividend Vault” worth more than $1.7 trillion. To learn more, including the name and ticker symbols of some of my favorite “Dividend Vault” stocks, click here.