The Easiest “Free Lunch” Way To Earn More On Your Cash Right Now…

This time last year, I told readers about the closest thing to a “free lunch” as you’ll ever see in investing.

I hope you listened.

In that article, I told you about Series I Savings Bonds, or I Bonds.

At the time, I Bonds offered investors a 3.54% rate or 7.12% annualized. That was the highest it had been in over a decade.

I was adamant that you should buy the bonds before April 30, 2022, because I was sure the rate would be even higher (thanks to soaring inflation) when the Treasury announced the new rate on May 1. (As a quick reminder, the rates change twice a year — May 1 and November 1.)

Sure enough, on May 1, 2022, the rate jumped to 4.81%, or 9.62% annualized. It remained there as inflation persisted until November 1, 2022. Then the rate dropped to an annualized rate of 6.89%, where it remains today. Although, the next rate change (May 1) will likely see this drop even lower.

The golden era of I Bonds is over… at least for now. Although, we shouldn’t scoff at a 6.89% rate. That’s still quite good. But for the trade-offs: having to lock up money for at least one year and a small limit ($10,000 per year, per person), I think there are better options out there.

Today, I will cover a few of those options and tell you what I’m doing with the extra cash I have.

A Great Environment For Cash

Banks got decimated by the Fed’s intense and furious interest rate hikes. But it’s also created a great opportunity for those with cash on the sidelines.

Thanks to the higher interest rates, that cash can actually work for us.

Capital One (NYSE: COF) has a savings account with a 3.5% interest rate. Citi Bank (NYSE: C) offers 3.85%. And many online financial institutions offer even higher. A quick Google search shows CFG Bank offering folks a 5% rate.

Heck, even Apple (Nasdaq: AAPL) announced (in partnership with Goldman Sachs) a high-yield savings account offering 4.15%.

So first and foremost, check with your bank and make sure you are in an account with the highest interest rate. You might be surprised to learn that many banks still pay out pitiful interest in savings accounts. The national average is just 0.37%.

For the first time in over a decade, consumers have the leverage against banks. If you have a good chunk of cash sitting at a bank, you can bet that they will work with you to offer the best rate they can. Now more than ever, banks do NOT want to lose deposits.

We Can Do Even Better Than That…

Now, if you’re willing to put in a little extra work, you can get an even better rate on your cash with U.S. Treasuries.

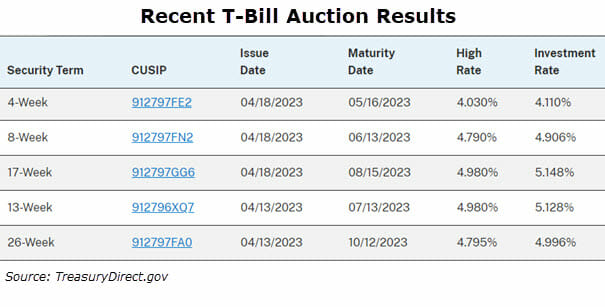

U.S. Treasuries are the debt obligations of the U.S. government. They are issued by the U.S. Treasury Department. Many people don’t realize you can easily buy Treasuries with durations as short as 30 days (4 weeks). These short-term Treasuries are referred to as “T-Bills.”

You buy these T-Bills at the same place you bought I Bonds: Treasurydirect.gov.

You can also buy T-Bills from your brokerage account. Of course, each brokerage has its own instructions for buying them, so it might be worthwhile to reach out to your brokerage’s customer service team to figure out how.

But it’s well worth it. I’ve bought on Treasurydirect.gov as well as through my brokerage account. My brokerage account only offers 0.35% on any cash that I don’t have invested. So, I bought some 4-week T-Bills and 8-week T-Bills. Now, I’m getting north of 4% on that 4-week T-Bill, and nearly 5% on the 8-week T-Bill.

A good strategy when buying T-Bills is to ladder your bond purchases. For example, you could buy some 4-week, 8-week, 13-week, and 17-week T-Bills. That way, you’re getting a bit better rate for the longer you lock up the money, but you also have money freed up every month or so that you can either reinvest or go out and blow it on something cool.

If you want to see the latest auction results on the various T-Bills, go here. Just make sure you click the PDF under “Competitive Results” to see the results of past auctions.

Now look, I understand that talking about bonds and T-Bills isn’t all that exciting. But it should be. We’re talking about making anywhere between 4x-40x more money on the cash that’s just sitting in our checking, savings, or brokerage accounts… darn near “risk-free.”

If you’re not doing this — making your cash work harder for you — then you are literally missing out on the second “free lunch” in investing that’s being offered right now.

An Even Easier Way To Make Your Money Work Harder

Okay, let’s say you don’t want to open a Treasury account… Or call your brokerage’s customer service to buy T-Bills there… Or call your bank to get a better interest rate (or change banks if that bank isn’t competitive).

There is another option…

You’re not going to get the best rate. But it’s as easy and simple as buying a stock. Just log into your brokerage account, type in the ticker symbol “BIL” and the SPDR Bloomberg 1-3 Month T-Bill ETF (NYSE: BIL) will pop up.

This ETF owns a basket of T-Bills with maturities of 3 months or less. As those bills mature, it delivers the interest earned to shareholders.

This short-term bond fund pays out dividends on a regular basis, typically at the start of each month. Its last dividend — paid April 10 — was $0.37 per share. Right now, the ETF sports a 2.4% dividend yield. But keep in mind that a big change in interest rates will increase or decrease that payout.

And like all ETFs, this one has an annual expense ratio. In this case, it’s 0.14%. So, you’ll pay a slight premium compared to buying via Treasury Direct. For some, that may be worth it to avoid the hassle of setting up a Treasury Direct account or buying them directly through your brokerage.

The other nice thing about this ETF is that you can quickly buy and sell shares. You don’t have to wait the full 30 or 60 or 90 days for your T-Bill to mature.

Closing Thoughts

The bottom line is that if you have cash sitting on the sidelines earning a pitiful 0.4% (roughly the national average), you need to do something about it.

Instead of relying on a bank to earn you interest, go out and be the bank of your own money. Buy some of these short-term T-Bills that are giving you anywhere between 3% and 5% interest. It’s a no-brainer.

P.S. It’s the biggest lie America has EVER been sold… And it’s about to destroy the retirement dreams of tens of millions.

America’s $2.8 trillion dollar “safety net” has a huge problem… And if Washington doesn’t act soon, it could set some retirees up to see a massive 23% “pay cut”. But that doesn’t have to be YOUR story…

That’s why I created a custom blueprint designed to generate up to $35,522 per year in EXTRA retirement income. That’s almost double the table scraps Social Security will toss to us in retirement. Go here to learn more…