3 Simple Steps To Take Charge Of Your Retirement Portfolio

A few days ago, I shared some rather grim statistics about how prepared the average American is for retirement.

A few days ago, I shared some rather grim statistics about how prepared the average American is for retirement.

As you can probably guess, it’s not looking good. After decades of stagnant wages and low savings rates, most Americans are woefully underprepared for retirement. And while it’s nice to have Social Security as a fallback, the truth is that it won’t bail most people out to the extent they think it will.

And if you don’t believe me, let me ask you this…

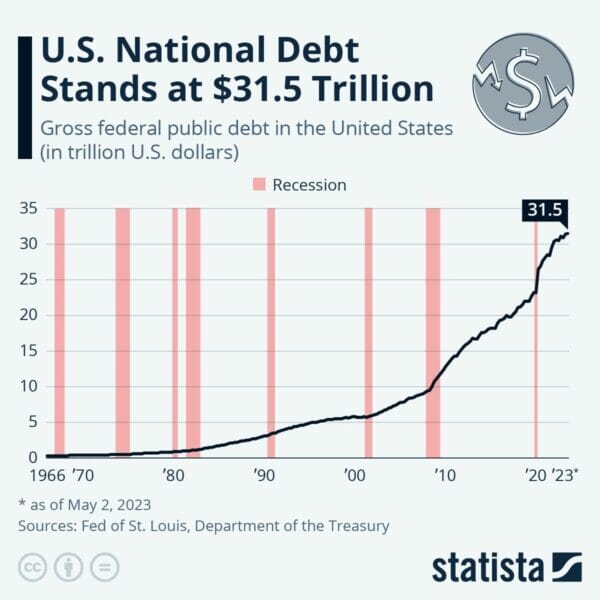

Do you think the same government capable of piling on $31.5 trillion of debt can fix Social Security? Personally, I’m a bit skeptical.

Source: Statista

Truthfully, I hate talking about politics when it comes to the market. But sometimes it’s unavoidable.

The growing debt pile is a big deal — and a bipartisan issue. Due to the Fed’s battle against inflation, higher interest rates will mean borrowing money will be even more costly. If something doesn’t change soon, we could be headed for a fiscal debt spiral that runs out of control.

My goal isn’t to scare you. And it isn’t to rant about things that are out of our control, either.

Quite the contrary. I bring all this up to tell you that you can’t count on anyone but yourself to achieve a comfortable retirement.

3 Steps To Put Your Portfolio On The Right Track

As Chief Investment Strategist of High-Yield Investing, I firmly believe blue-chip, dividend-paying stocks and other high-quality interest-bearing securities remain the best way to achieve that goal.

That’s why I want to skip the gloom and doom today and focus on offering solutions. To that end, I want to take a step back and talk about some of the basic steps investors can take to set their portfolios up for long-term success.

So, if you’re looking to get started (or simply need to get back on track), I would start with these three simple steps…

1. Determine Your Needs

Some people have modest retirement agendas. They might be able to get by on 50% to 60% of their pre-retirement income levels. Others plan to live large… golfing, traveling, you name it. In that case, it’s better to plan on needing perhaps 70% to 80% of your former income or possibly more.

Other variables must be considered, such as anticipated inflation rates (the enemy of anyone living on a fixed income). $50,000 in annual withdrawals might sound ample today, but you can bet it won’t buy nearly as much 20 years from now.

Just to give you an idea, picture a couple in their mid-40s who want to retire at age 60 with $60,000 in annual retirement income until age 78. Ignoring Social Security (we’ll count that as a bonus) and assuming a 4% yield in retirement, they will need to accumulate a starting balance of $990,741 by day one.

It’s not an exact science, and there is no accounting for the unknown. But at least you’ll be making an educated guess as to how much you’ll need to accommodate your expected retirement lifestyle.

2. Start Saving NOW!

Once you know how much cash you’ll need before you can stop punching the clock, the next step is to make a ballpark projection of your current portfolio’s worth. Be careful about assuming lofty double-digit rates of return.

Despite a sometimes-bumpy ride along the way, the stock market has treated us very well over the past few years. But personally, I wouldn’t count on the market delivering more than 8% annually over the long haul. If you actually earn more than that, great… you’re ahead of the game. But it’s better to aim lower and beat that than to come up short. If you’ve been a diligent saver until now and continue to save aggressively, your projected account value might outpace your projected needs.

But for most people, there will be a sizeable gap. Don’t let that be you.

3. Rebalance Annually

You might not realize it, but the biggest determinant of your long-term returns isn’t the individual performance of the stocks, bonds, and mutual funds you select. It isn’t market timing, either.

A groundbreaking study involving 94 mutual funds over 10 years found something interesting. About 90% of an investor’s ups and downs are due to the overall mix and proportion of various asset classes within their portfolio. So the best use of your time is deciding on asset allocation… deciding what percentage to invest in large-cap stocks versus small-caps, growth versus value, domestic versus foreign, equity versus fixed income, cash, gold, real estate, etc.

Customize your asset allocation strategy for your unique goals and objectives. Providing hand-tailored profiles to thousands of different readers here just isn’t practical. But a moderate-risk allocation for investors in their 50s might look something like this:

- 30% Investment Grade Bonds

- 25% Large-Cap Blend

- 10% High-Yield Bonds

- 10% Floating Rate/TIPS/Inflation Protected Bonds

- 10% Global Stocks

- 5% Real Estate/Commodities

- 5% Small/Mid-Cap Value

Whatever you decide, it’s important to re-evaluate at least annually. This is a good opportunity to cut loose any laggards that aren’t performing to your expectations and re-align allocations that got out of whack over the previous year.

In most cases, you’ll also want to dial back your exposure to riskier asset classes as you approach retirement. At that point, you should be less concerned with capital appreciation and more interested in capital preservation.

Closing Thoughts (Plus Bonus Tips)

Remember, what I’ve told you today is just the beginning. There’s more to consider. To that end, I’ve included links to a few recent articles that discuss some important tips to help you along the way:

Bonus Tips

- Understand how compounding and reinvesting dividends can make you rich over time.

- Yield isn’t everything (here and here).

- You can’t go wrong with Dividend Aristocrats.

- Money market funds are a no-brainer for your cash right now.

Taking the time to come up with a game plan is one thing. Having the diligence to stick with it is another thing entirely. But it can mean the difference between a lean retirement and a lavish one.

Don’t feel overwhelmed; any plan is better than doing nothing. If nothing else, dollar-cost averaging (buying fewer shares when prices are high and more when prices are low) into a solid mutual fund each month can take you a long way.

P.S. Tired of waiting around for your dividends to come in every quarter? How does getting paid every month sound?

If that sounds too good to be true, think again. In this eye-opening report, you’ll learn about 12 ultra-generous dividend payers that put more money in your pocket every month. Go here now.